This content is provided for informational and educational purposes only, and should not be relied upon as legal, business, investment, or tax advice. Furthermore, references to any securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Factomind cannot be responsible for your use of the information provided in this content. Factomind has established, maintained, and enforced strict internal policies and procedures designed to identify and effectively manage conflicts of interest related to its business activities. Factomind does not own any digital assets mentioned below, nor has it made any purchases or sales of the digital assets mentioned below. All materials in this research paper are sourced from publicly available information.

1. Introduction

We have witnessed thousands of blockchains and dApps that proclaimed to onboard the next wave vanish, and after all this time everyone still calls for ‘mass adoption.’ How far are we on the adoption meter, and how large of an audience are we selling into? How large of a user base are we supposed to accumulate in order to be a top DeFi contender?

Especially with all these DeFi projects popping up ever since 2020, we wonder if the market allows how many projects to proliferate, or justifies the valuation for a single project–Uniswap. In this paper, we will quantify the demand side of on-chain finance and size the market.

Simple addresses could be a crude proxy to the actual demand, but it would be vastly inaccurate considering the amount of MEV bots parasitic (both in good ways and in bad ways) to organic users. We will introduce the concept of derived demand, which is existent if and only if the primitive demands are present, and filter out the derived demands to gauge the true size of the primitive demands, or the actual users of DeFi protocols.

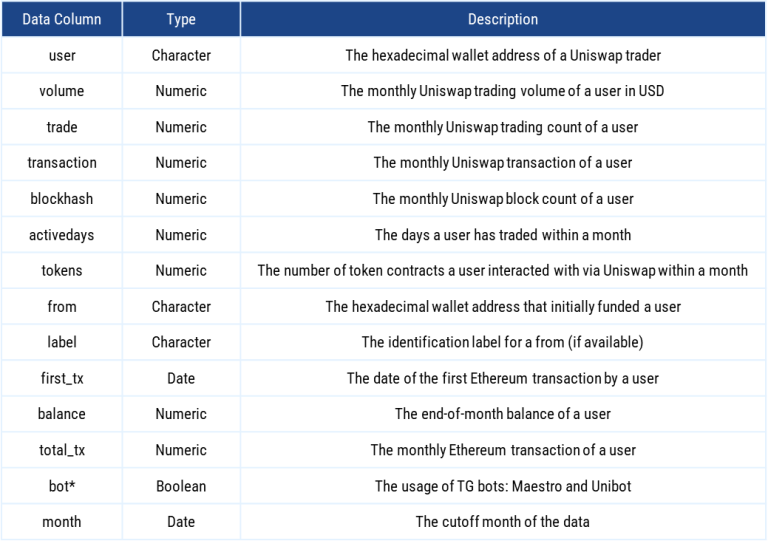

2. Data Specification

We gathered the following data columns from the Ethereum blockchain about Uniswap users from 2020.06 to 2023.06.

Table 1 – Data Description

*Note that Boolean bot is different from the MEV category below. For a matter of fact, “bot” in this sense is classified as Core Primitive users, or true organic users of Uniswap.

3. Model

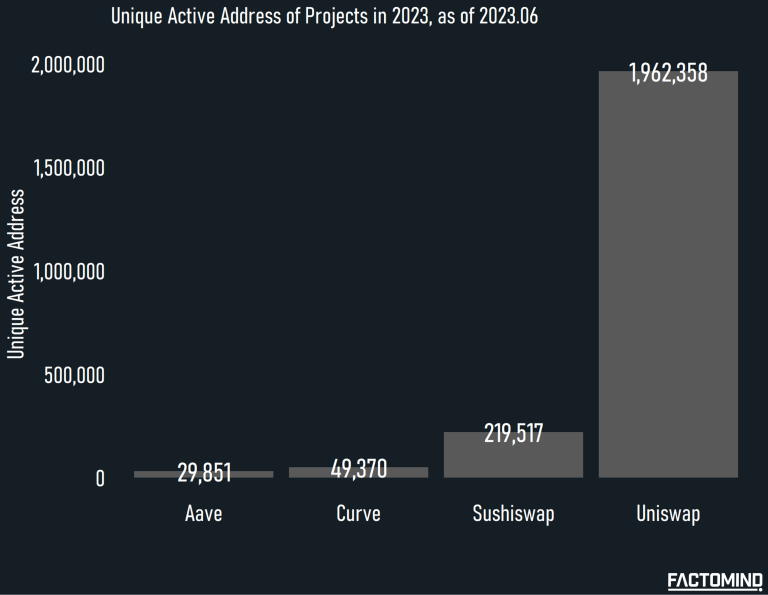

Under the objective of estimating the true size of the on-chain finance industry, we established the following hypotheses and methods. We limited our scope of study to Uniswap because it has by far the most active addresses which are mostly overlapping with other protocol users, thus it serves well to be a comprehensive representation of the on-chain finance market.

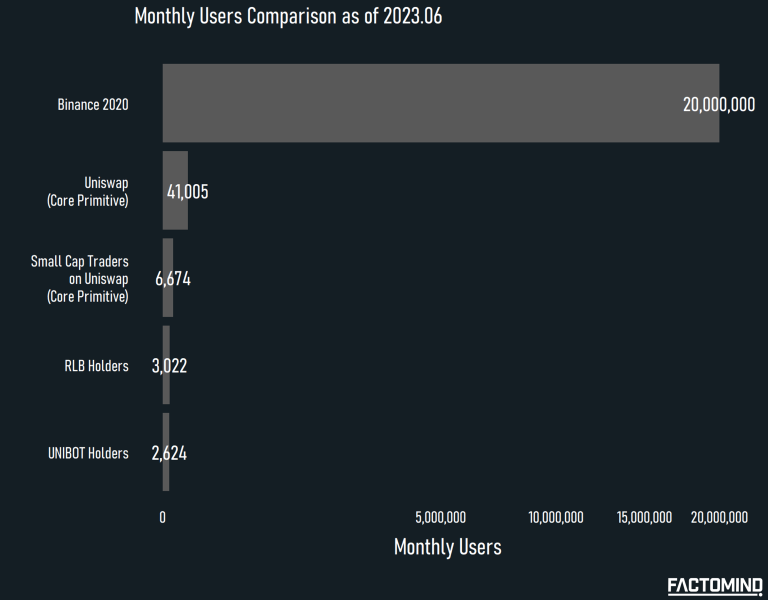

Figure 1 – Unique Active Address of Projects in 2023, as of 2023.06

Even among the most predominant protocols on the Ethereum blockchain, Uniswap stands out in terms of active addresses according to Figure 1. Therefore, we deem it reasonable to extrapolate the Uniswap users as the proxies of the on-chain finance demand.

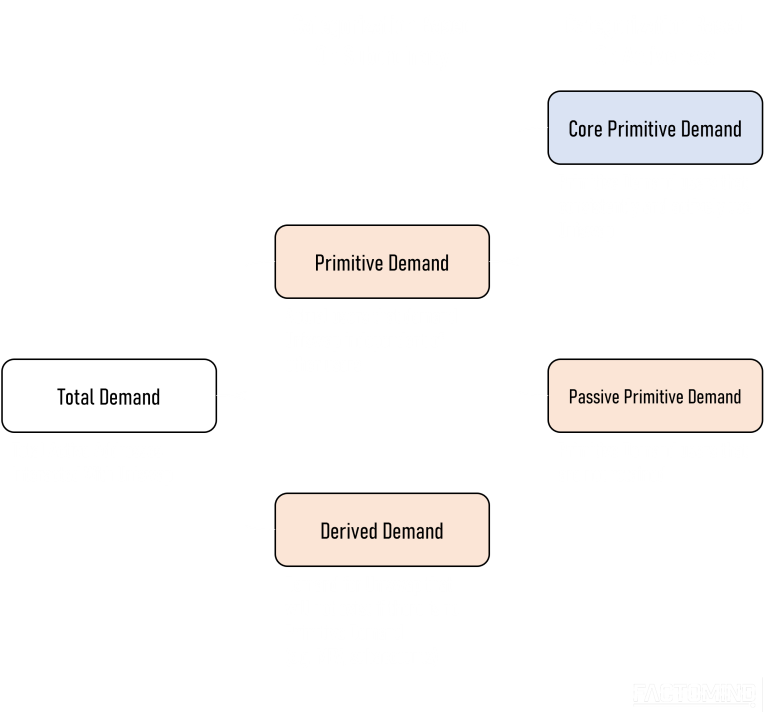

3.1. Hypotheses

We assume that there are two types of demands in terms of demand subordinacy, and also in terms of activeness.

Figure 2 – On-chain Finance Demand Categorization For Uniswap

Total Demand is the total addresses that interacted with Uniswap.

Primitive Demand is the actual users that organically and independently demand Uniswap irrelevant of other users.

Derived Demand is the demand for Uniswap that only exists when Primitive Demand exists. MEV Bots and subaccounts belong to this category.

Core (Primitive) Demand represents the active, retained users of Uniswap, and thus will be our core target for filtering.

Dormant (Primitive) Demand is the demand, although Primitive, that is not retained or barely makes transactions on Uniswap.

Our core goal is to filter our other noises to gauge the true size of Core Primitive Demand. Do note that we are not verifying whether there are real humans sitting behind Core Primitive Demand accounts; for example, an actively trading Unibot account will be categorized as Core Primitive as somebody is deploying a bot to demand Uniswap, which is an actual demand (whether they are for sniping, flipping, or buy and hold).

However, MEV bots only trade if and only if Core Primitive Demand accounts trade, thus they are classified as Derived Demand.

3.2. Filtering Methodology

We utilized 4 distinct logics to filter out Derived Demand and Dormant (Primitive) Demand. Note that all data are from Uniswap.

Filters for Derived Demand

MEV Filter : Transaction Count to Block Count > 1.1 OR Transaction Count in Top 0.5% percentile We introduced the above condition to MEV bots that push more than one transactions within a single block for arbitrage or sandwich attacks

Subaccount Filter : Funded from the same non-CEX or non-smart contract wallets A self-explanatory condition to filter out subaccounts; we labeled the Subaccount filtered wallets with the highest activity as Primitive

Filters for Dormant (Primitive) Demand

Being active for at least 3 months in a 6 month lookback (or >50% of the months for accounts with less than 6 months age) AND

More than 3 Swap transactions in each of the active months

4. Chasing the Uniswap – Data Overview

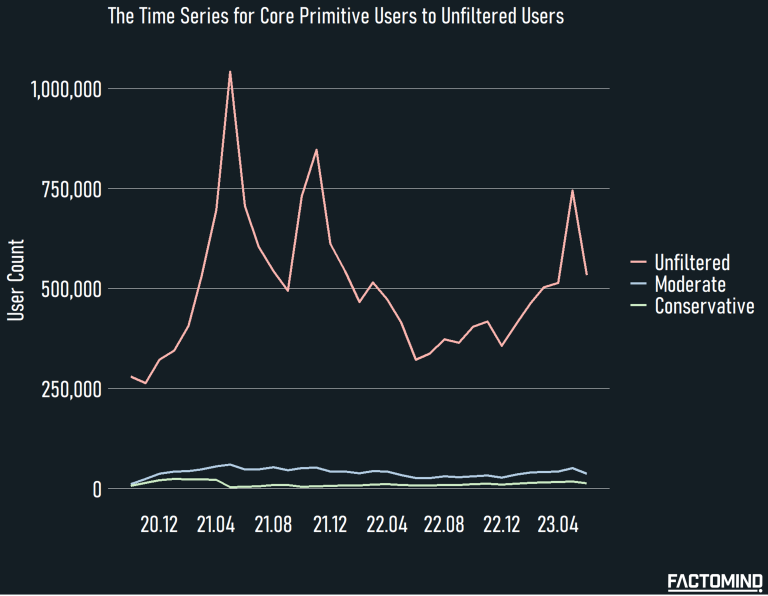

Our findings suggest that although the monthly active addresses for Uniswap hovers above 600K, the Primitive Core Demand–or actual users demanding Uniswap–is much less at 40K for a moderate case and at 10K for a conservative case.

A moderate case of 40K is the direct result of applying the filtering methods described in 3.1.

A conservative case of 10K is applying the duplicated ratio of 20% from Subaccount Filter to CEX funded wallets as well, under the unlikely assumption that CEX funded wallets are also flooded with subaccounts.

Figure 3 – The Time Series for Core Primitive Users to Unfiltered Users on Uniswap

As mentioned above, ‘Conservative’ assumes that the subaccount ratio of CEX funded wallets is equal to EOA-funded wallets, which is a quite harsh assumption. Thus, Moderate would be our base case from hereunder.

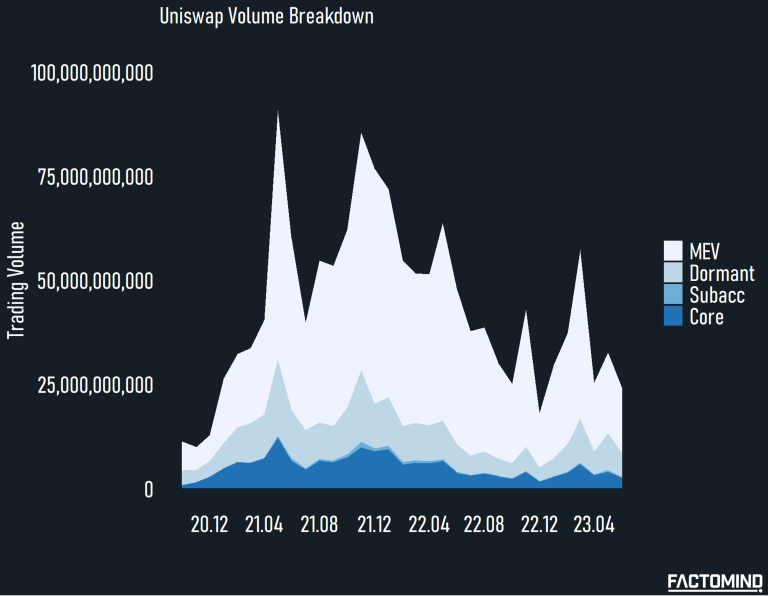

Figure 4 – Uniswap Volume User Category Breakdown

*Trading volume hereunder is denoted in dollar terms.

Figure 4 is a mere reconfirmation of a widely known fact that the majority of trading activity comes from MEV. We did not distinguish types of MEV as they are beyond the scope of this paper.

Table 2 – User Category Summary

Table 1 summarizes the key statistics of Core Primitive category users.

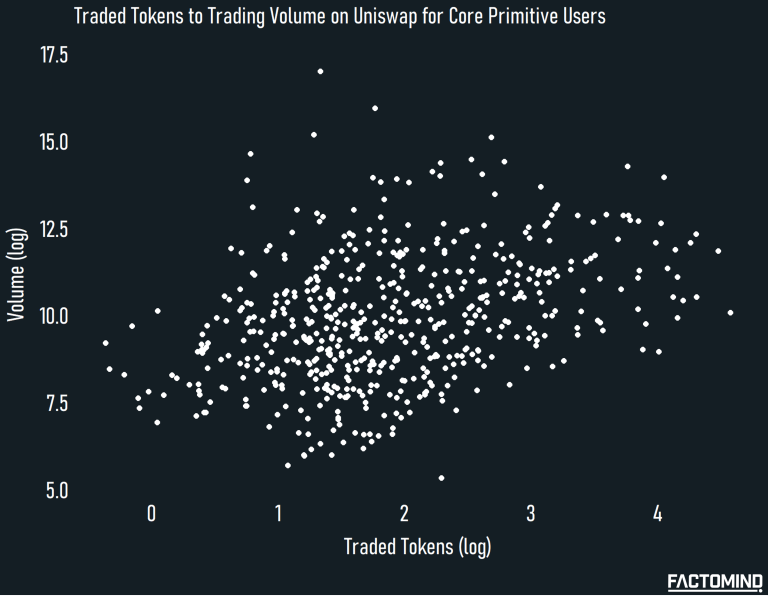

Figure 5 – Monthly Average Traded Tokens to Trading Volume on Uniswap per Core Primitive User

Trading volume is very loosely correlated with traded tokens with a correlation of 0.09, which is not surprising considering the majority of the trading volume on Uniswap is concentrated to a few top pairs—namely, ETH-USDC/USDT and USDC-USDT.

5. Chasing the Uniswap – Stylized Facts

5.1. A Ghost Town for DeFi

Less than 10% of the current active addresses on Uniswap are Core Primitive users, making the monthly active DeFi user estimate between 10K and 40K.

The majority of the wallets are Dormant (Primitive) users, which are created, send a few transactions, and then disappear.

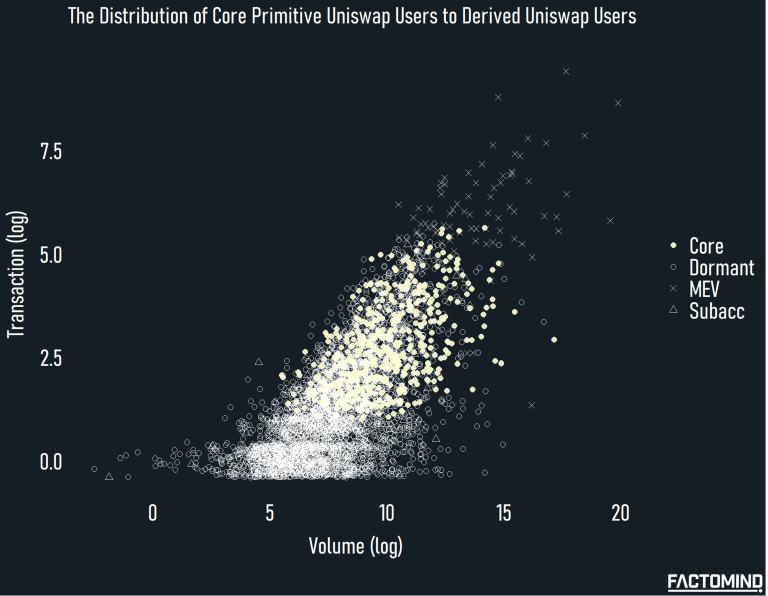

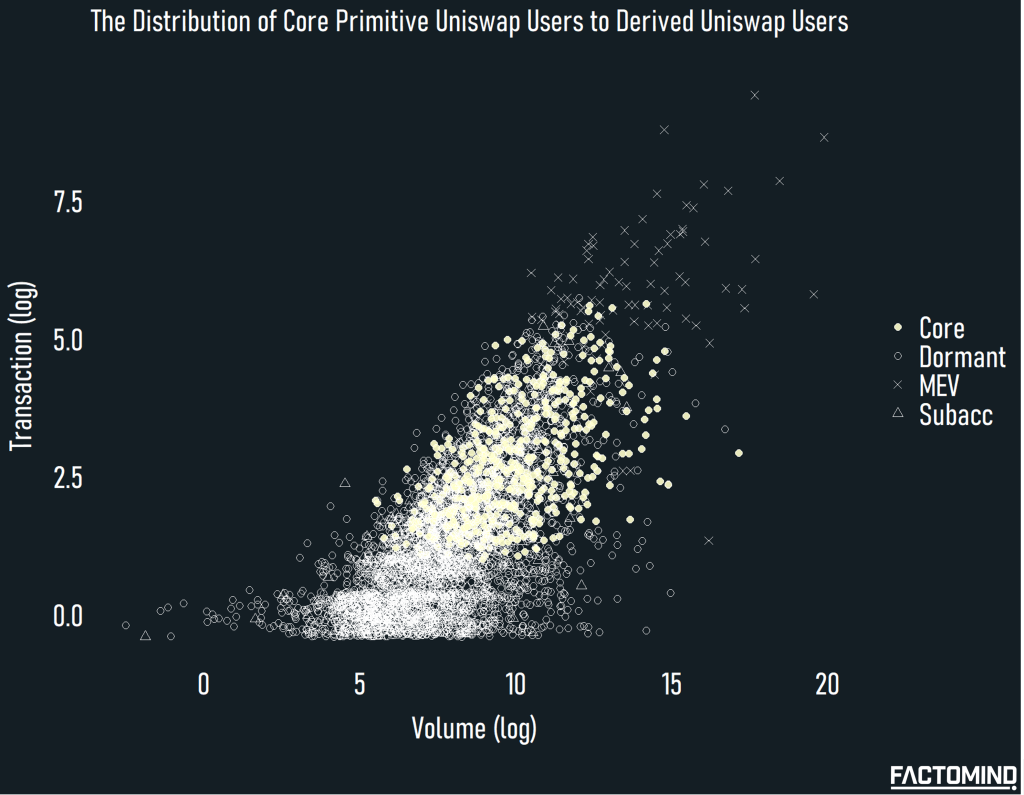

Figure 6 – The Distribution of Core Primitive Users to Derived Uniswap Users

While most active addresses are Dormant, most trading volume is generated from MEV Bots, which are Derived Demand that is parasitic to Core Primitive users (again, MEVs are not necessarily bad).

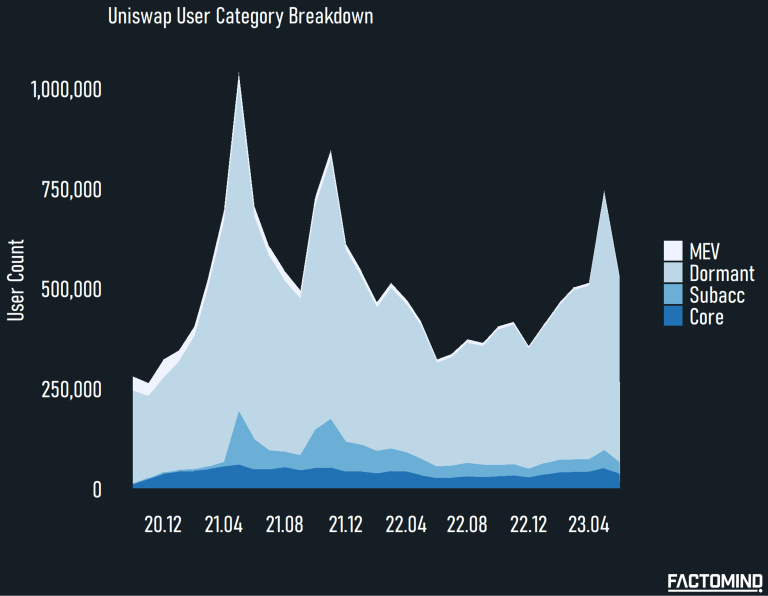

Figure 7 – Uniswap User Category Breakdown

If we look at the overall time frame, we can easily notice that the majority of upticks in Uniswap users is attributable to inflows of subaccounts and Dormant users (non-retained flash users). An interpretation could be that the booming cycles in the Web3 industry entice new users enough to try on-chain finance, yet the utility is insufficient to keep them around.

5.2. To Whom Your Token Sells

CEX listings are sometimes notorious for producing ‘selling pressure,’ yet without CEX listings, projects are basically selling their tokens into a 6K people market.

Among the 40K monthly Core Primitive Uniswap users as of 2023, only 6,474 users actively trade Small Cap* tokens. Considering the $RLB holders and $UNIBOT holders amount to ~3K after the recent surge, we believe our estimates are reasonable as these two projects are not listed in any major exchanges as of writing.

*For simplicity, we assumed the Core Primitive Uniswap users who interacted with 10+ token contracts to be Small Cap traders

Although $RLB and $UNIBOT are both successful projects uniquely positioned in their areas, their token holder outreach falls short compared to other recent CEX listed projects such as $PEPE (130K holders) or $BLUR (40K holders).

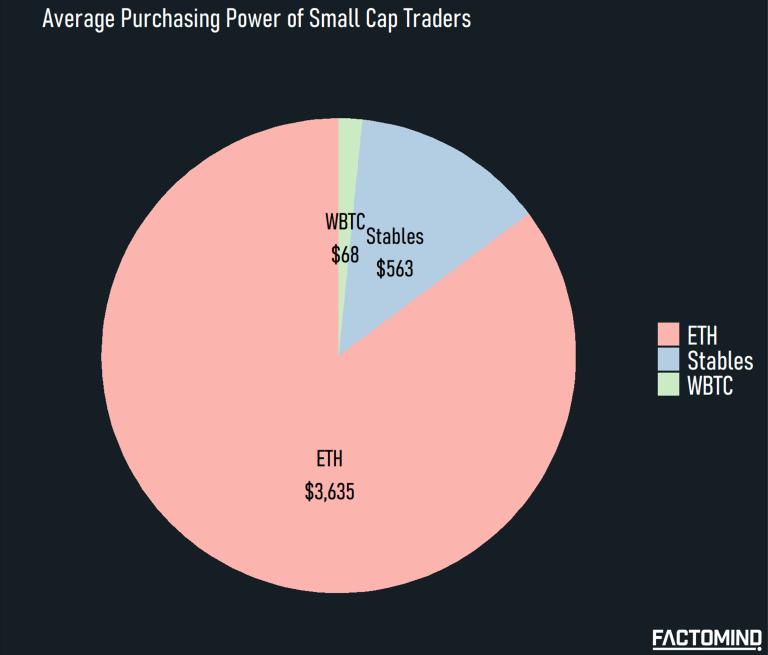

Figure 9 – Purchasing Power of Small Cap Traders on Uniswap

On average, the Small Cap traders hold roughly $4K of tradable assets in their wallets, mostly in $ETH.

5.3. No Market for Young Men (Once You Go Bull, You Never Go Dull)

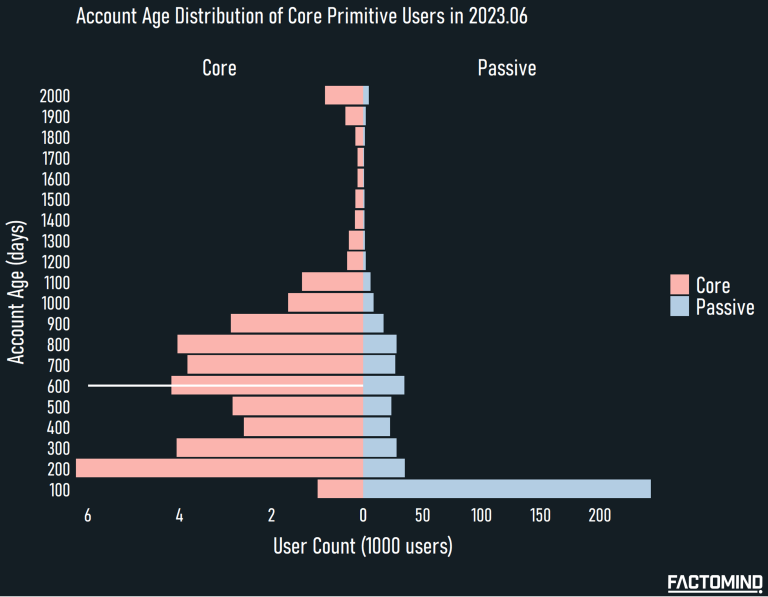

Median account age for Core users in 2023 is 600 days, while the median account age for Dormant users is 200 days, suggesting that the retained, active users are the old users who used Uniswap since 2021, while newcomers try out Uniswap once or twice then leave.

It is a finding that coincides with 5.1. A Ghost Town in DeFi.

Figure 10 – Account Age Distribution of Core Primitive Users in 2023.06

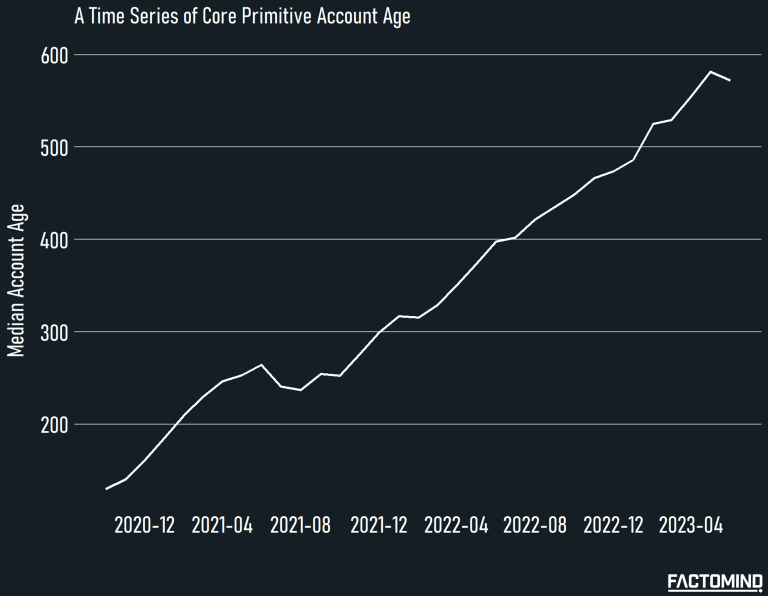

If we look at the average account age of the Core Primitive users in a time series, we can see that it is a non-stop upward trend, meaning OGs keep returning to Uniswap, yet YGs are barely retained.

Also note that while the most new users are not retained, denoted by the huge blue bar at the bottom, yet the next wave of onboarded users are within (100, 200] days range, where the flickering sign of a bull market was lit with $BTC and $ETH price rallying nearly 50%.

Figure 11 – A Time Series for Core Primitive Account Age

The prolonged plateau in the year 2021 might be a good omen that an exuberant bull market could excite newcomers to be onboarded to blockchains.

5.4. Time Can’t Break Bonds But It Can Break Funds

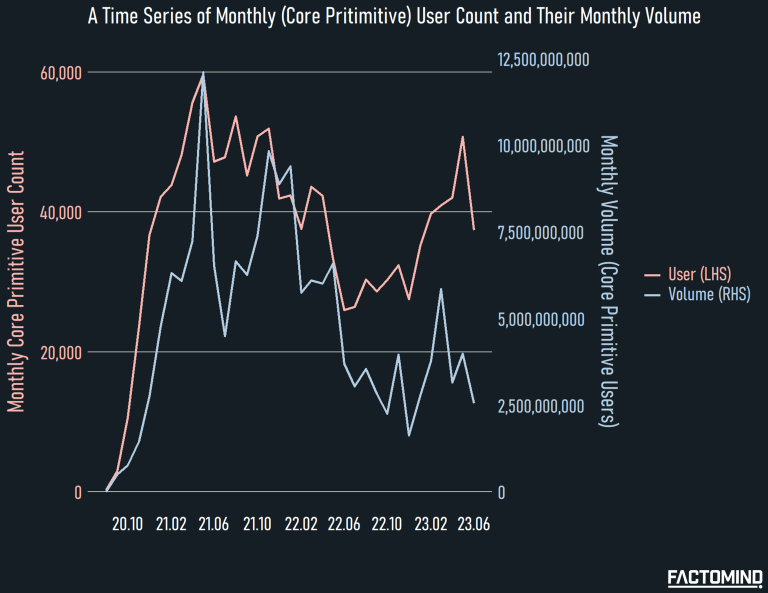

After 2 years since the euphoric bull run in 2021, we have recovered back to the 2021 level in the Core Uniswap user terms; however, their average trading volume is significantly smaller than in the 2021.

While the Core users in 2023 are 85% of the 2021 level, their trading volume is a meager 32%.

Figure 12 – A Time Series for Monthly User Count and Monthly Volume

5.5. Ride the Tide of Bullish Pride

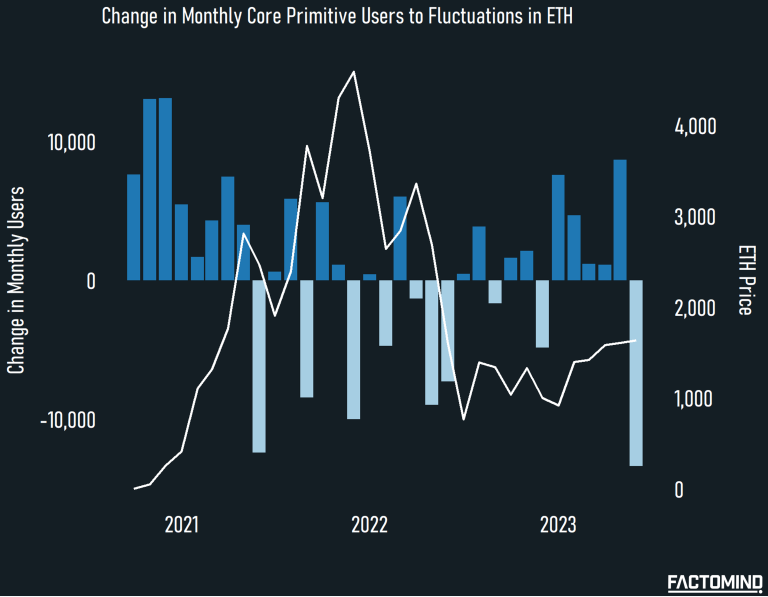

Bull markets drive users in, and bear markets do the opposite. This could be a sign that the majority of on-chain finance is still limited to investment purposes.

Figure 13 – Change in Monthly Core Primitive Users to Fluctuations in ETH

5.6. Options Galore in a Meme Lore

Despite the market being more bearish compared to 2021, the number of products in the market and the tokens traded by Core Primitive users are at the highest level since the inception of Uniswap, possibly owing to the recent Memecoin plays and TG bot narratives.

Figure 14 – Average Tokens Traded by Core Primitive Users

5.7. ENS : Evidently Not Swapping

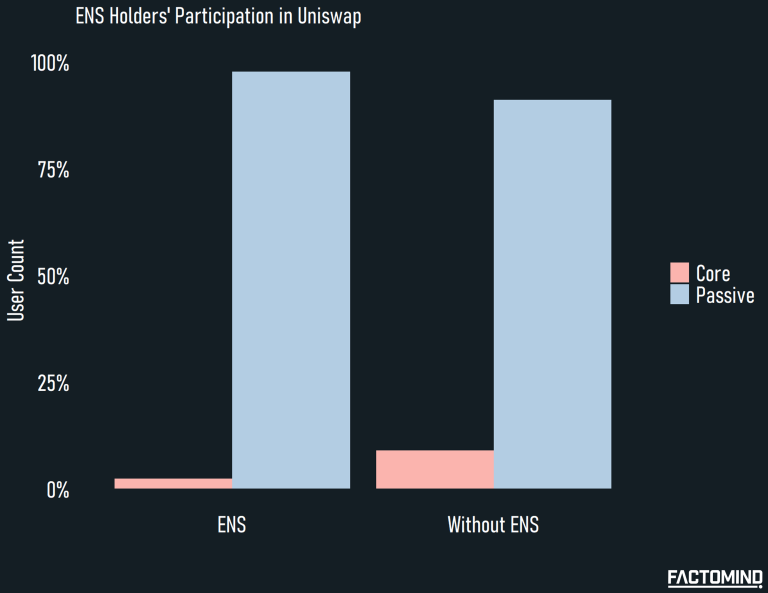

ENS holders, despite the common conception that holding ENS names is representative of the fervent participation in on-chain activities, are actually much less active on Uniswap compared to Non-ENS holders.

Figure 15 – ENS Holders’ Participation in Uniswap

6. Summary and Key Takeaways

– There are 600,000 monthly unique traders (wallets) on Uniswap.

– Out of 600,000 monthly unique traders, approximately 40,000 are real, organic users (which we dubbed ‘Core’) that are not MEV bots, subaccounts, or dormant addresses.

– Out of 40,000 real, organic users, approximately 6,000 traders actively trade tokens other than $ETH and stablecoins.

– We are essentially selling our business into these 6,000 small cap traders for on-chain finance projects, unless we go for CEXes for a better reach.

This gives us two insights:

1) This is not an absurd number that requires tremendous funding in marketing, the number is within reach with a decent product paired with a decent strategy.

2) With only 6,000 active participants on the on-chain finance market, we still have much room to grow.