So far our paper series revolved around the fungible universe, covering topics ranging from community building to business goal setting. There is the other asset class looming in the corner, the non-fungible buddies. We have intentionally prioritized fungible tokens as they occupy the majority of the Web3 market cap and are more actively traded. Yet, we have never neglected NFTs, and from now on we will release a paper series dedicated to the NFT market.

All our Thematic Research Series share one core theme—we share insights derived from market data. Before extracting meaningful insights from data, we must refine it to remove the impact of distortions, so that we draw a clear, undistorted picture of the market. Often, as we filter the dataset, we discover new market perspectives which were unavailable before.

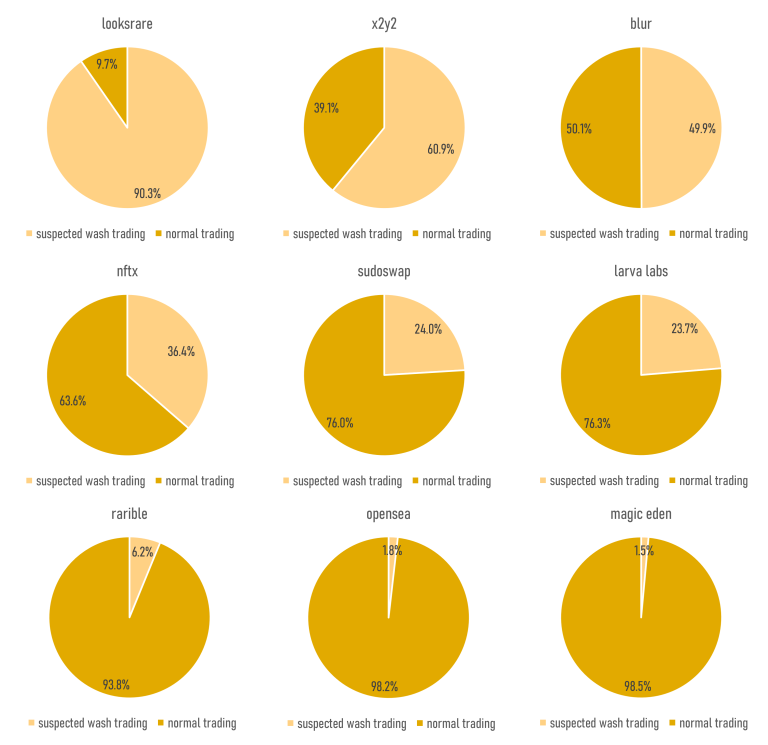

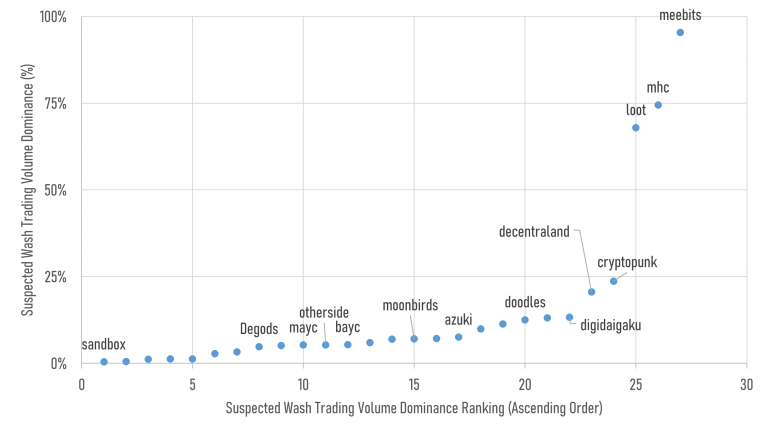

One of the prevalent, yet serious market challenges is wash trading behavior. Wash trading in the fungible market (and also in the TradFi market) is done to spread misleading information to other market participants, particularly about the attractiveness of a project’s token. Failure to adjust for such a faulty intelligence results in a critical error to anyone participating in the market. Thus, we filter our database for market distortions to provide an accurate representation of the market status.

In the NFT market, filtering data for wash trading is even more important than in fungibles due to two core reasons. One, all NFTs possess unique Token IDs, allowing us for token-based analyses, whereas for fungible ones, only account-based analyses are allowed. Two, NFT markets are much more vulnerable to market anomalies due to illiquidity.

For our first part of our NFT series, we prepared an inclusive paper on NFT wash trading—how and why do traders use wash trading, and what are the expected consequences? Spoiler alert, the current NFT market is greatly overestimated.